Learning goals for this section: I want you to become familiar with the tools that are available to you and how they work so that you can craft your own personal financial system.

Introduction

In the first part of this series, but only in abstract terms with the goal of helping you build a mental model of personal finance and what it can do for you.

Once you have a good understanding of personal finance as a system that you can shape and mold, you need to understand how to do those things. What are the tools you can use and how do they work? I will be going into the nitty gritty in this part of the series.

An Emergency Fund

The world is wildly unpredictable and emergencies will happen. Before you create a complex system, you need to make sure your system can withstand these emergencies. The simplest way to do this is to establish an emergency fund. An emergency fund is a set amount of money that you never touch unless an emergency occurs.

Typically you can hold this fund in your savings accounts. Alternatively, you can open up a separate savings account in which you contain this money.

The amount of money you hold in your emergency fund is subjective. Some people are more conservative than others and try to have at least one years worth of spending (rent, groceries, medical costs) in their emergency fund. Some are less conservative and only have three months. My personal suggestion is to have at least 3 months in your emergency fund as a bare minimum, I would encourage you to slowly build your emergency fund up to at least 6 months of runway. This will allow you to still pay rent and bills if you lose your job and need time to find another.

As I mentioned, you need to build an emergency fund before you do anything else. No personal financial system is safe without a bulwark against unpredictable markets or life events. Once you have established a minimum emergency fund, it’s time to start looking to other boxes to add to your system.

The 401k

Introduction

Limit: $19,500 per year

The 401k is the most commonly known investment tool for working people. The 401k is a retirement account that is provided by your employer.

I’m not going to tell you what to invest in (just yet), instead I want to explain how a 401k works and why it’s a powerful tool to add to your system. Let’s break this down into really simple parts first.

Explanation

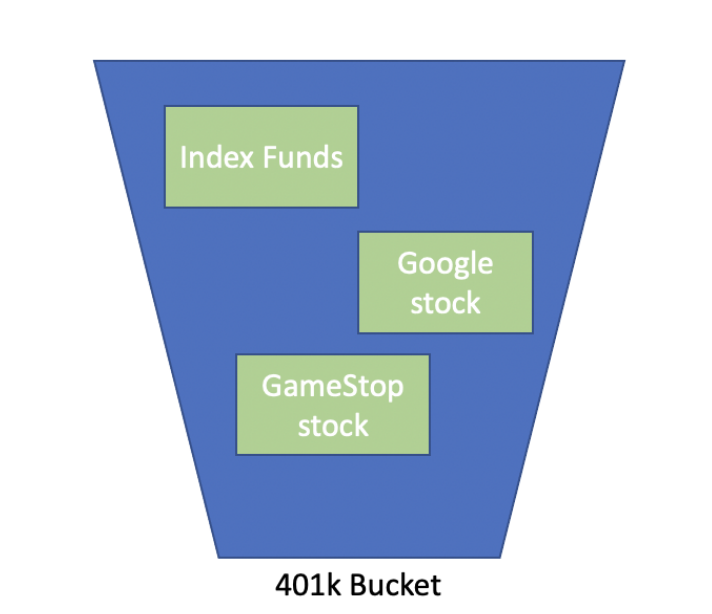

Your 401k isn’t an investment itself. Instead, it is a bucket (account) that holds investments inside of it. You can have multiple different investments inside one 401k. Here is an example picture:

Your 401k is a retirement account. Since it is itended for use when you are retired, you can only access the money inside your 401k when you’re 59 years old. Investments do best when you leave them for long periods of time and the 401k forces you to do this. Even though it’s the “responsible” thing to do, it still seems really boring and kind of a bad deal. Well, there are some really rad things about the 401k that make it a pretty sweet deal.

Sweet Deal #1 : The Company Match

Typically, when you input money into your 401k, your employer will match a certain amount of your input. Meaning if you put in $1,000, your employer may match that amount and put an extra $1,000 into your account. You have literally doubled your money before you’ve even done anything.

Different companies have different matching policies, figure out yours.

Sweet Deal #2 : Tax Benefits

So there are two types of 401Ks, the Traditional 401k and the Roth 401k.

In the Traditional 401k, the money you invest from your salary is invested before you pay taxes on your salary (pre-tax). Here is a simple example: If you make $50,000 a year and you invest $19,500 dollars into your 401k, you will be only taxed on your income as if you had made $30,500 a year. That’s pretty cool because you will pay less in income tax.

In the Traditional 401k, you don’t pay taxes on the money you invest. Instead you pay taxes when you take money out of the 401k. This means that when you’re old and retired, the money you take out of your 401k counts as income, and you will need to pay income tax on it when you’re old.

The Roth 401k is the exact opposite. Your money is invested into the 401k after you pay taxes on your salary. So for the previous example if you made $50,000 and invested all $19,500, you would still be taxed as if you made $50,000.

The benefit to the Roth 401k is that you don’t have to pay taxes when you withdraw the money when you’re old

The type of 401k you choose is up to you and your personal situation. If you aren’t making a ton of money right now, it may be best to invest in a Roth 401k as you wouldn’t currently benefit from being taxed on a lower income currently, but you would benefit from not having to pay taxes later.

In the end, I personally don’t think it matters all that much. Yes it matters and it is something to think about, but it is better to invest in a sub-optimal way than to not invest at all. If you really can’t decide, choose the Traditional 401k and call it a day.

Example and a Graph

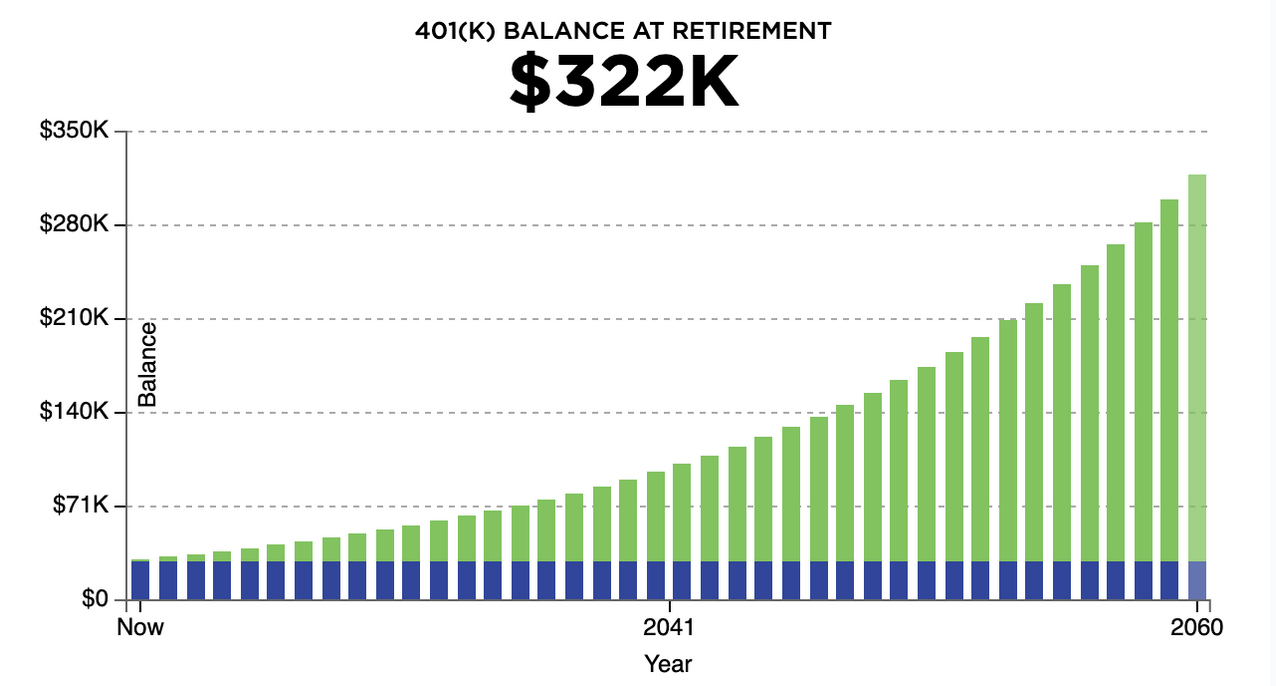

The 401k is insanely powerful. To demonstrate, let’s say you only invested $19,500 one time when you were 25. If your employer matches 50% of your contributions, they will contribute $9,750 for a total of $29,250. Let’s say you never invest another cent into your 401k. Here is a graph that would show your returns at a 6% rate of return. At the age of 65 you would have $322,000 in your 401k just based on you putting $19,500 in your 401k one time 40 years ago!

Just imagine the growth if you continue to invest over the course of your life. If you take it seriously at an early age, you will reap some insane rewards.

Bottom line, invest in your 401k damnit.

The IRA

Limit: $6,000 per year Income Limit: You need to make less than $140,000 a year to invest in an IRA

Explanation

Similarly to the 401k, the IRA is a retirement account but it is not provided by your employer. Instead you need to open one up for yourself through a brokerage firm (Fidelity or Vanguard).

The IRA works similarly to the 401k in that there are two types: Traditional IRA, and Roth IRA. The difference between these two is the same as the difference between the Traditional and Roth 401k, it’s all about when you get taxed.

My personal recommendation is to invest in a Roth IRA for simplicity sake. It’s easier to invest post-tax money without having to fiddle with stuff come tax time. Plus all of the growth is tax-free.

Similarly to the 401k, you can’t take this money out until you are 59 years old.

The Weird Parts

Let me clarify, you can’t take out the earnings of your IRA until your 59, but you can take out your contributions at any time (stupid idea though).

So if you invest $6,000 into your account, it will grow over time. But at any time you can take that $6,000 out without having to pay a penalty. Don’t do this though, it’s a really stupid idea.

The Brokerage Account

The brokerage account is just an account in which you can invest money. There is no retirement schtick here, it’s just straight up investing. Since there’s no retirement aspect to this account, there aren’t any cool tax advantages.

Brokerage accounts are hosted by brokerage firms such as Fidelity or Vanguard. You can go to either of these firms and open up an account. Once it’s open, you can use the account to invest in different things whether it be bonds, index funds, or specific stocks.

Since there are no tax advantages here, it should be one of the last things you put money in. You have to invest money after tax and you have to pay taxes whenever you take money out (sell investments). Therefore, you should first max out your 401k and IRA before you pour money into a brokerage account.

Conclusion

In this section I went over the most common accounts including retirement accounts and brokerage accounts. I only scratched the surface of these investment account types, I encourage you to learn more if you’re interested but I’ve provided enough information for you to get going.

If you’re interested, here are some other components you can add to your personal financial system that are beyond the scope of this document:

- HSA (Health Savings Account, can be used as a retirement account)

- 529 Plan (Investment account you can use to pay for education)